-

Get the latest news! Subscribe to the ifa bulletin

Get the latest news! Subscribe to the ifa bulletin

In debates around what represents good risk advice, many proposals are suggesting that only level premiums should exist in the future.

This is alarming given that non-insurance-based factors may result in a level premium recommendation transpiring to be very poor advice – something I have experienced first-hand.

Several years ago I was working as an aspiring paraplanner and sought to obtain some long-term cover.

I met with an adviser and was recommended a comprehensive solution, funded with 'level' premiums to take advantage of my age at application date.

This was poorly-considered advice as no thought had been given to the foreseeable future where I would likely progress to an adviser and obtain a better occupation code.

I decided on a 'stepped' premium variation and two years later, re-wrote the cover with a level premium under a superior occupational category. This decision will save me tens of thousands of dollars over the life of the policy (not to mention the one-thousand dollar saving each year whilst I was a cash-poor paraplanner).

Level premium recommendations are often based on advisers seeking to ‘lock away’ the best insurance terms available today.

As clients’ premiums increase with age, locking away insurance terms for a 35-year-old may insulate them against significant premium hikes throughout their 40s and beyond. This approach is very straightforward, but more thought is required.

When recommending level insurance premiums advisers must also consider if the insurance terms recommended will remain the best option in the foreseeable future.

It may be over 10 years before your client gets any tangible benefit from your ‘level’ premium recommendation and a wide range of both predictable and unpredictable events can occur over this time.

Before you recommend any level premium, consider the following:

• Career progression: Is your client likely to be in a considerably better occupational code in the coming years? This becomes a key question for aspiring professionals, as mentioned earlier, but give thought to other scenarios such as tradesmen with successful and growing businesses.

Are they still going to be ‘on the tools’ in 5-10 years, or running the business from their home office, with incidental hands-on work? It’s also important to know if your client is considering a career change in the future: not just in the next 12 months but over the next 5-plus years.

• Anticipated windfalls: Are there any one-off funds likely to be received in the future? A client with ill or elderly parents may be receiving a significant benefit at some point in the future; naturally this type of windfall is highly unpredictable but it is reasonable for you to take a long-term view.

Given that paying stepped premiums for 10-15 years may still work out cheaper than paying level premiums over the same timeframe, a stepped approach may be optimal if any windfall would be expected to eliminate the need for your recommended cover.

• Future plans for your client: Taking a 10-15-year approach, some clients may have the surplus income to clear all their debts beforehand – and perhaps the debts that you were seeking to cover with your level premium insurance recommendation.

Will the clients continue to grow their wealth through borrowing (for instance via investment properties or business debt) or will all debt be cleared to pave the way for a long-term savings strategy?

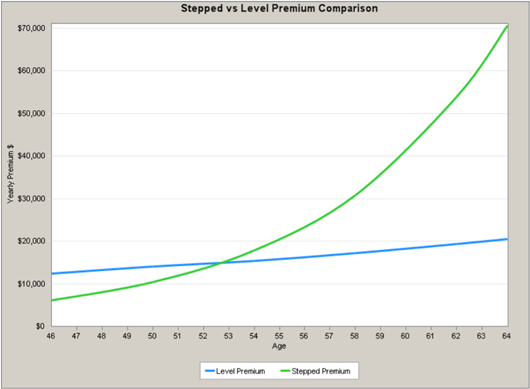

Lastly, consider the utility of money which is used to fund a higher (level) insurance premium over the long term. The graph below represents a 'stepped' vs 'level' comparison for a 45-year-old professional:

The 'crossover point' occurs in year 8, and the decision to take out a 'level' premium achieves a net benefit in Yr 14.

But what if short-term savings achieved by using stepped premiums were invested with compound interest? Assuming a 6 per cent return, this would equate to over $35,000, kicking the true 'crossover point' much further down the path.

If your increased level premium costs resulted in the client being unable to clear long-term personal loan or credit card debt, this recommendation may significantly disadvantage them financially.

As with many aspects of financial advice, these decisions require the adviser to ask the right questions and show a good deal of financial leadership.

Career progression can’t be forecast with certainty, nor can your clients’ future financial intentions, but after detailed assessment, ‘the balance of probabilities’ should be considered.

Level premiums often have their place in a comprehensive insurance solution but recommending the right premium structure needs thorough consultation with clients and more thought around the foreseeable future.

James O'Reilly is the co-founder of Verse Wealth

Never miss the stories that impact the industry.