-

Get the latest news! Subscribe to the ifa bulletin

Get the latest news! Subscribe to the ifa bulletin

Since the National Disability Insurance Scheme (NDIS) was launched to test sites around the country in July this year, it has been recognised as a significant milestone for disabled Australians, their carers and families.

Since the National Disability Insurance Scheme (NDIS) was launched to test sites around the country in July this year, it has been recognised as a significant milestone for disabled Australians, their carers and families.

Blogger: Katherine Ashby, Senior Product Technical Manager, BT Financial Group

However, there are concerns the title, ‘Disability Insurance’, does not accurately describe the program, and with a large percentage of Australians being underinsured, there remains a serious potential for further complacency if the scheme is not properly understood.

Since the launch of the scheme, insurers have received a small number of calls from policyholders to cancel their income protection, total and permanent disability (TPD) and trauma insurance, due to the understanding that they would now be covered under a government safety net.

From July 2014, the number of queries from policy holders is expected to increase as the Medicare levy rises from 1.5 to 2% to partially fund the scheme – meaning all Australians will see their take home pay packets reduce to fund the “Disability Insurance Scheme”.

Due to the potential substantial changes to the livelihood of some people as a result of the scheme, in order to provide adequate information for clients, advisers should be acutely aware of the following:

Who does it cover?

Eligibility for coverage is based on three requirements; namely, age, level of disability and residency. Participants are required to be under the age of 65 when they become disabled, as well as when joining the program. Once in, lifetime coverage is provided.

In order to meet residency requirements, participants are required to live in an area covered by the scheme. Participants are also required to be permanently disabled, meaning their social and economic participation in the community is hampered.

Who misses out?

Participants already aged 65 or over, or due to turn 65 before their region is covered, will not be eligible to participate in the scheme. In addition, anyone with a temporary and/or curable disability, such as mental health, diabetes and cancer, will not be eligible, unless no other possible remedies are made available.

At this stage, the scheme is not means tested.

What does the scheme provide?

Eligible participants will have the opportunity to work with a case worker to develop a specialised support plan, which may include equipment or home modifications, support with household tasks, transportation, therapies and assistance with entering the workforce.

Financial advisers should be aware of the following support information, as it differs from general insurance needs analyses.

As the Disability Support pension will continue to provide financial assistance, monetary assistance or income support will not be provided through the NDIS. The cost of medical treatment is covered by Medicare, and will not be included in the benefits of the scheme.

Timeline

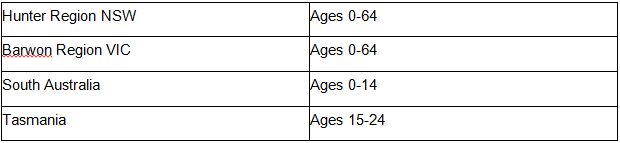

All states and territories have now signed up to the scheme, with the sites below launching in July this year. The states that signed up first were given preference for launch sites. In conjunction with the federal government, the states decided on the scope, limiting the launch to certain segments either by region or age.

Additional sites will begin in the ACT, NT and Western Australia in July 2014, while Queensland is yet to announce an official launch date.

The scheme will roll out slowly, but progressively, with NSW being the first state with full coverage due in July 2018. All other states are expected to have full coverage by July 2019, meaning people aged 59 years and over may never receive coverage.

The NDIS has bipartisan support, with no major changes to the proposal expected in the foreseeable future. The program provides a welcome improvement in the level of assistance previously available for people with disabilities; however, for the life industry in particular, advisers need to ensure they continue to educate policyholders and the general public about the difference between a welfare program and comprehensive personal insurance.

About Katherine Ashby

BT's Katherine Ashby is the Senior Product Technical Manager in the Life Insurance team. She provides specialised support and analysis on regulatory change, advice strategies and technical aspects of life insurance

BT's Katherine Ashby is the Senior Product Technical Manager in the Life Insurance team. She provides specialised support and analysis on regulatory change, advice strategies and technical aspects of life insurance

Never miss the stories that impact the industry.